What Happens If You Miss ITR Filing Deadline in India?

Introduction

Filing your Income Tax Return (ITR) on time is not just a legal requirement—it is essential for maintaining financial credibility and avoiding penalties. However, many taxpayers miss the deadline due to lack of awareness, poor planning, or confusion.

In this article, we explain what happens if you miss the ITR filing deadline, penalties involved, and how you can still file your return legally.

📜 Legal Framework for ITR Filing

Under the Income-tax Act, 1961, filing of returns is governed by:

- Section 139(1) – Due date for filing ITR

- Section 139(4) – Belated return

- Section 234F – Penalty for late filing

- Section 234A – Interest on delayed tax payment

These sections define what happens when deadlines are missed.

⏰ What is the ITR Filing Deadline?

For most individuals:

- Due date: 31st July of the assessment year

For businesses requiring audit:

- Due date: 31st October

Missing these deadlines triggers penalties and restrictions.

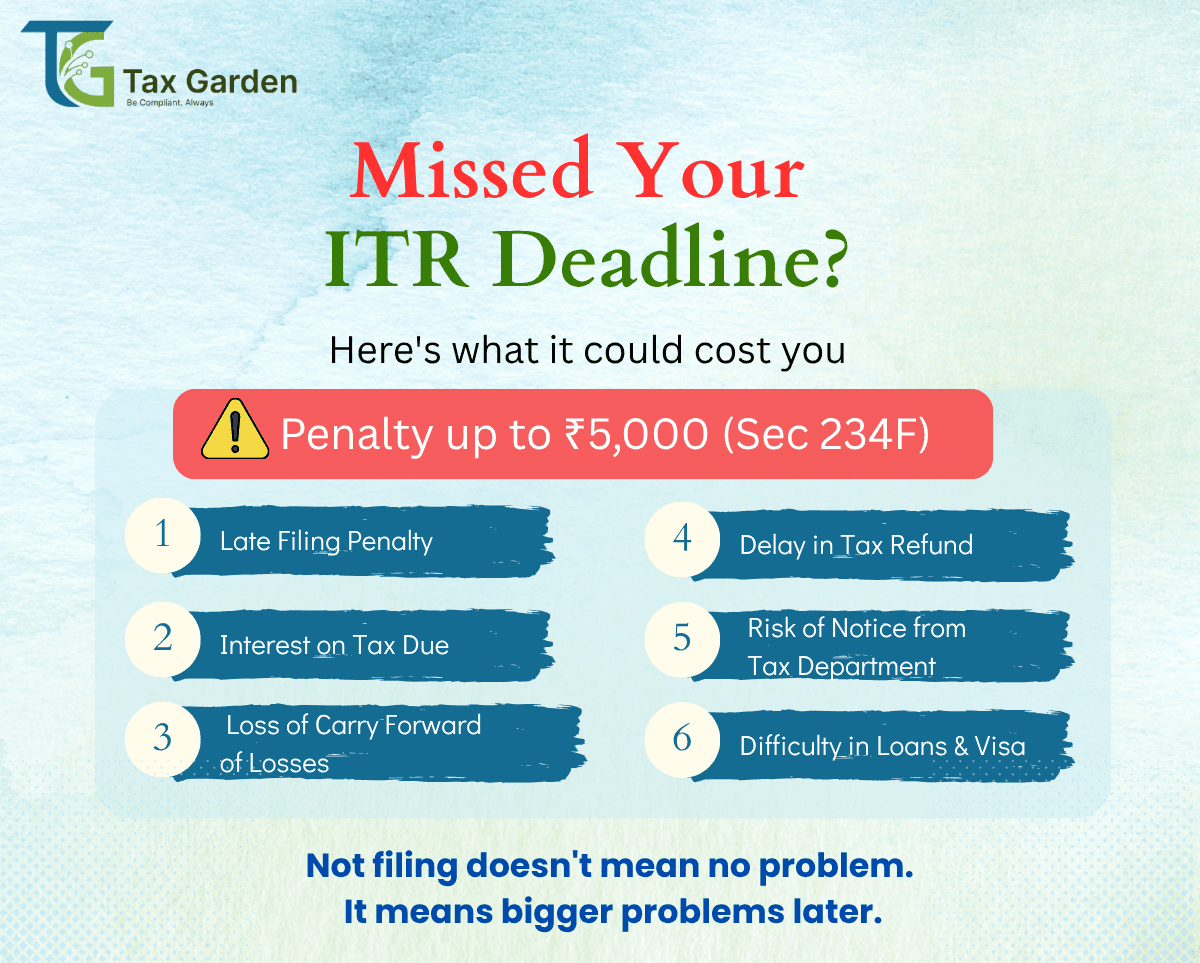

🚨 Consequences of Missing ITR Deadline

1️⃣ Late Filing Penalty

Under Section 234F:

- ₹5,000 → if filed after due date but before 31st December

- ₹1,000 → if income is below ₹5 lakh

- ₹10,000 → (older rule; currently capped effectively at ₹5,000 for most cases)

2️⃣ Interest on Tax Due

Under Section 234A:

- Interest at 1% per month on unpaid tax

- Calculated from due date till actual filing date

👉 Even 1-day delay = full month interest.

3️⃣ Loss of Carry Forward of Losses

If you file late, you cannot carry forward losses, such as:

- Business losses

- Capital losses

This can cost you huge tax savings in future years.

4️⃣ Delay in Tax Refund

If you are eligible for refund:

- Filing late → refund gets delayed

- No penalty for refund cases, but cash flow impact

5️⃣ Risk of Notice from Tax Department

The Income Tax Department of India tracks:

- Bank transactions

- TDS records

- AIS (Annual Information Statement)

If return is not filed:

👉 You may receive compliance notices.

6️⃣ Difficulty in Loans & Visa

ITR is used as financial proof for:

- Bank loans

- Credit cards

- Visa applications

Missing filing → reduces financial credibility.

🔁 Can You Still File ITR After Deadline?

Yes 👍

Under Section 139(4), you can file a Belated Return.

Time Limit:

- Up to 31st December of assessment year

Example:

For FY 2024–25 → File till 31 Dec 2025

⚠️ What If You Still Don’t File?

Serious consequences:

- Penalty notices

- Prosecution in extreme cases

- Additional fines

- Scrutiny by tax department

🧠 How Government Tracks Non-Filers?

Modern system uses:

- AIS (Annual Information Statement)

- TDS data

- PAN tracking

- Bank & digital transaction monitoring

👉 Even if you don’t file, your income is already visible to the system.

✅ How to Avoid Missing ITR Deadline

- Set reminders before July

- Maintain income records monthly

- File early (June–July)

- Consult a tax professional

- Use online filing portals

💡 Pro Tip for Tax Garden Audience

Even if your income is below taxable limit:

👉 Filing ITR is still useful for:

- Building financial history

- Easy loan approvals

- Claiming refunds

📌 Conclusion

Missing the ITR filing deadline may seem like a small mistake, but it can lead to penalties, interest, and financial limitations. The good news is that the law still allows you to file a belated return within a specific time frame.

Understanding the provisions of the Income-tax Act, 1961 helps you stay compliant and avoid unnecessary losses.

👉 The best strategy is simple: File early, stay stress-free, and remain compliant.

Missed Your ITR Deadline?

Our tax experts can help you file a belated return, minimize penalties, and stay compliant with income tax regulations.